Ito vs Stratonovich

This script is an implementation of a really simple stochastic ODE to show the difference between Ito and Stratonovich calculus. Please note that this script defines functions at the end, which is only supported by MATLAB 2016b or later.

Contents

the SDE has the form:

Ito calculus is handled by the standard Euler Maruyama scheme:

Stratonovich calculus is handled by the Euler Heun scheme:

![$$ x^n+1=x^n + f(x^n,t^n) \Delta t + \Delta W*[g(x^n,t^n)+g(\bar{x},t^n)]/2. $$](stoch_ito_stratonovich_eq04649210088799611819.png)

Note that for additive noise g is a constant so the two are the same.

The Stratonovich interpretation effectively adds a drift.

clear all, close all % Initialize the random number generator and seed it. rng('shuffle');

Specify the global parameters.

mysig=1; myper=3e-2;

Specify the time step and stochastic parameters.

numsteps=10; numouts=100; dt=1e-5; dtrt=sqrt(dt); dtb=dt*numsteps; dtbrt=sqrt(dtb); numens=4000;

Set up arrays for storage and store initial state.

t=0; xs=zeros(numouts+1,numens); xi=zeros(numouts+1,numens); x0=zeros(1,numens); xs(1,:)=x0; xi(1,:)=x0; xd=x0(1);x=x0;x2=x0; ts(1)=t; cntr=0; xs(1,:)=x; xds(1)=xd; ts(1)=t;

Primary loop

for ii=1:numouts

for jj=1:numsteps

cntr=cntr+1;

noisenow=randn(1,numens);

Euler Maruyama.

x=x+dt*sin(2*pi*t/myper)+dtrt*mysig*noisenow.*atan(x)*(2/pi);

Euler-Heun.

x2bar=x2+mysig*noisenow.*atan(x)*(2/pi);

x2=x2+dt*sin(2*pi*t/myper)+0.5*dtrt*mysig*noisenow.*(atan(x2bar)*(2/pi)+atan(x2)*(2/pi));

t=t+dt;

end

Storage

xs(ii+1,:)=x2;

xi(ii+1,:)=x;

ts(ii+1)=t;

end

Plotting

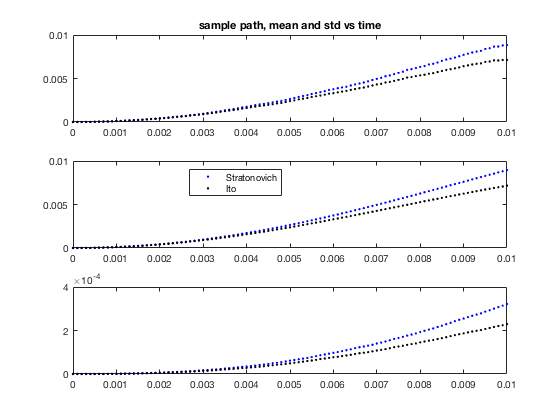

Plot one path, mean and standard deviation.

figure(1) clf subplot(3,1,1) plot(ts,xs(:,1),'b.',ts,xi(:,1),'k.') title('sample path, mean and std vs time') subplot(3,1,2) plot(ts,mean(xs,2),'b.',ts,mean(xi,2),'k.') legend('Stratonovich','Ito','Location','best') subplot(3,1,3) plot(ts,std(xs,[],2),'b.',ts,std(xi,[],2),'k.')

Derivative-free Milstein Method Ito

function x_next = dfmil_ito(x_n,f_n,g_n,h) x_bar = x_n + feval(f_n,x_n)*h + feval(g_n,x_n)*sqrt(h); x_next = x_n + feval(f_n,x_n)*h + feval(g_n,x_n)*sqrt(h)*randn + 0.5*h^(-0.5)*(feval(g_n,x_bar)-feval(g_n,x_n))*(h*randn^2-h); end

Derivative-free Milstein Method Stratonovich

function x_next = dfmil_strat(x_n,f_n,g_n,h) x_bar = x_n + feval(f_n,x_n)*h + feval(g_n,x_n)*sqrt(h); x_next = x_n + feval(f_n,x_n)*h + feval(g_n,x_n)*sqrt(h)*randn + 0.5*h^(-0.5)*(feval(g_n,x_bar)-feval(g_n,x_n))*(h*randn^2); end